It’s a data point that is widely and openly presented as fact—not only by those inclined to dismiss the current system as inadequate (or worse), but even by some of its most ardent champions, who see it as a call to action for expanded access to these programs. It’s drawn from the U.S. Census Bureau’s March 2012 Current Population Survey (CPS).(1) But does it tell the full story?

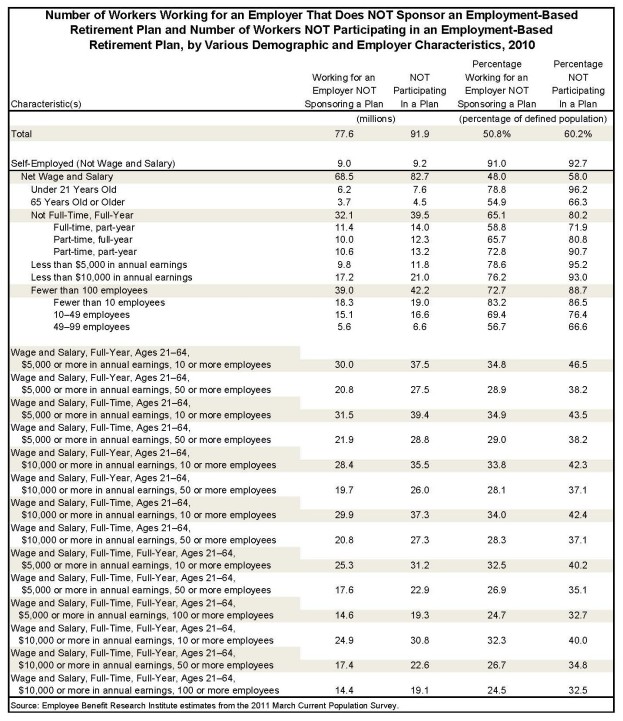

A recent EBRI Issue Brief notes that in 2011, 78.5 million workers worked for an employer/union that did not sponsor a retirement plan. Looking specifically at those who did not work for an employer that sponsored a plan, the report notes that:

- 8.9 million were self-employed (and were thus barred from having a plan by their own inaction).

- 6.2 million were under the age of 21 (below ERISA’s mandated coverage level).

- 3.9 million were age 65 or older (beyond “normal” retirement age).

- Just over 31 million were not full-time, full-year workers.

- 16.8 million had annual earnings of less than $10,000.

When you filter out the overlap between those categories—situations where workers fall into several of those categories simultaneously (for example, workers who are under age 21, have less than $10,000 in annual earnings, and who are not a full-time, full-year worker)—there are about 42.4 million workers whose lack of coverage might be attributed to being in one or more of those categories. And yes, that’s more than half of the “uncovered” workers in the CPS analysis.

Indeed, while claiming that “fewer than half of working Americans have access to a workplace retirement plan” might be technically accurate, doing so exaggerates the size of the coverage “gap”—and obscures factors that might actually help explain it.

Nevin E. Adams, JD

(1) A similar result can be gleaned from the National Compensation Survey from the Bureau of Labor Statistics.

(2) There are other factors linked to rates of participation. For example, the EBRI Issue Brief also notes a correlation between firm size and participation. See Figure 30 in “Employment-Based Retirement Plan Participation; Geographic Differences and Trends, 2010.”

No comments:

Post a Comment